Kindly share you feedback about the website – Click here

GENERAL INSTRUCTIONS:

1. This question paper contains 34 questions. All questions are compulsory.

2. This question paper is divided into two parts, Part A and B.

3. Part – A is compulsory for all the candidates.

4. Part – B has two options i.e.

(i) Analysis of Financial Statements and

(ii) Computerised Accounting. Students must attempt only one of the given options as per the subject opted.

5. Question Nos.1 to 16 and 27 to 30 carries 1 mark each.

6. Questions Nos. 17 to 20, 31and 32 carries 3 marks each.

7. Questions Nos. from 21 ,22 and 33 carries 4 marks each

8. Questions Nos. from 23 to 26 and 34 carries 6 marks each

9. There is no overall choice. However, an internal choice has been provided in 7 questions of one mark, 2 questions of three marks, 1 question of four marks and 2 questions of six marks.

PART A

(Accounting for Partnership Firms and Companies)

1. A & B are partners sharing profits and losses in the ratio of 3:2. C is admitted for ¼ and for which ₹30,000 and ₹10,000 are credited as a premium for goodwill to A and B respectively. The new profit-sharing ratio of A:B:C will be:

a) 3:2:1 b) 12:8:5 c) 9:6:5 d) 33:27:20

View AnswerAns. d) 33:27:20

2. Assertion: Batman, a partner in a firm with four partners has advanced a loan of ₹50,000 to the firm for last six months of the financial year without any agreement. He claims an interest on loan of ₹3,000 despite the firm being in loss for the year. Reasoning: In the absence of any agreement / provision in the partnership deed, provisions of Indian Partnership Act, 1932 would apply.

a) Both A and R are correct, and R is the correct explanation of A.

b) Both A and R are correct, but R is not the correct explanation of A.

c) A is correct but R is incorrect.

d) A is incorrect but R is correct.

View AnswerAns. d) A is incorrect but R is correct.

3. If 10,000 shares of ₹10 each were forfeited for non-payment of final call money of ₹3 per share and only 7,000 of these shares were re-issued @₹ 11 per share as fully paid up, then what is the minimum amount that company must collect at the time of re-issue of the remaining 3,000 shares?

a) ₹ 21,000 b) ₹ 9,000 c) ₹ 16,000 d) ₹ 30,000

View AnswerAns. b) ₹ 9,000

OR

On 1st April 2022, Galaxy ltd. had a balance of ₹8,00,000 in Securities Premium account. During the year company issued 20,000 Equity shares of ₹10 each as bonus shares and used the balance amount to write off Loss on issue of Debenture on account of issue of 2,00,000, 9% Debentures of ₹100 each at a discount of 10% redeemable @ 5% Premium. The amount to be charged to Statement of P&L for the year for Loss on issue of Debentures would be:

a) ₹30,00,000. b) ₹22,00,000. c) ₹24,00,000. d) ₹20,00,000.

View AnswerAns. c) ₹24,00,000.

4. A, B and C who were sharing profits and losses in the ratio of 4:3:2 decided to share the future profits and losses in the ratio to 2:3:4 with effect from 1st April 2023. An extract of their Balance Sheet as at 31st March 2023 is:

At the time of reconstitution, a certain amount of Claim on workmen compensation was determined for which B’s share of loss amounted to₹5,000. The Claim for workmen compensation would be:

a) ₹15,000 b) ₹70,000 c) ₹50,000 d) ₹80,000

View AnswerAns. d) ₹80,000

OR

A, B and C are in partnership business. A used ₹2,00,000 belonging to the firm without the information to other partners and made a profit of ₹35,000 by using this amount. Which decision should be taken by the firm to rectify this situation?

a) A need to return only ₹2,00,000 to the firm.

b) A is required to return ₹35,000 to the firm.

c) A is required to pay back ₹35,000 only equally to B and C.

d) A need to return ₹2,35,000 to the firm.

View AnswerAns. d) A need to return ₹2,35,000 to the firm.

5. Interest on Partner’s loan is credited to:

a) Partner’s Fixed capital account.

b) Partner’s Current account.

c) Partner’s Loan Account.

d) Partner’s Drawings Account.

View AnswerAns. c) Partner’s Loan Account.

6. Alexa Ltd. purchased building from Siri Ltd for ₹8,00,000. The consideration was paid by issue of 6%debentures of ₹100 each at a discount of 20%. The 6% Debentures account is credited with:

a) ₹10,40,000 b) ₹10,00,000 c) ₹9,60,000 d) ₹6,40,000

View AnswerAns. b) ₹10,00,000

OR

Which of the following statements is incorrect about debentures?

a) Interest on debentures is an appropriation of profits.

b) Debenture holders are the creditors of a company.

c) Debentures can be issued to vendors at discount.

d) Interest is not paid on Debentures issued as Collateral Security.

View AnswerAns. a) Interest on debentures is an appropriation of profits.

7. Assertion (A) :- A Company is Registered with an authorised Capital of 5,00,000 Equity Shares of ₹10 each of which 2,00,000 Equity shares were issued and subscribed. All the money had been called up except ₹2 per share which was declared as ‘Reserve Capital’. The Share Capital reflected in balance sheet as ‘Subscribed and Fully paid up’ will be Zero.

Reason (R) :- Reserve Capital can be called up only at the time of winding up of the company.

(a) Both Assertion (A) and Reason (R) are Correct and Reason (R) is the correct explanation of Assertion (A)

(b) Both Assertion (A) and Reason (R) are Correct, but Reason (R) is not the correct explanation of Assertion (A)

(c) Assertion (A) is incorrect, but Reason (R) is Correct.

(d) Assertion (A) is correct, but Reason (R) is incorrect

View AnswerAns. (a) Both Assertion (A) and Reason (R) are Correct and Reason (R) is the correct explanation of Assertion (A)

8. G, S and T were partners sharing profits in the ratio 3:2:1. G retired and his dues towards the firm including Capital balance, Accumulated profits and losses share, Revaluation Gain amounted to ₹ 5,80,000. G was being paid ₹ 7,00,000 in full settlement. For giving that additional amount of ₹ 1,20,000, S was debited for ₹ 40,000. Determine goodwill of the firm.

a). ₹ 1,20,000 b). ₹80,000 c). ₹2,40,000 d). ₹ 3,60,000

View AnswerAns. c). ₹2,40,000

OR

Annu, Banu and Chanu are partners, Chanu has been given a guarantee of minimum profit of ₹8,000 by the firm. Firm suffered a loss of ₹5,000 during the year. Capital account ofBanu will be ________ by₹_________.

a) Credited, ₹6,500. b) Debited, ₹6,500. c) Credited, ₹1,500. d) Debited, ₹1,500.

View AnswerAns. b) Debited, ₹6,500.

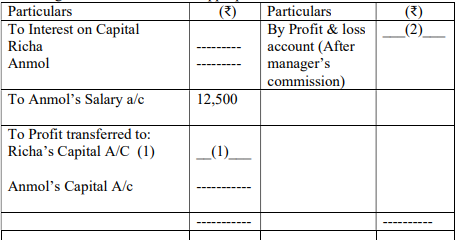

Read the following hypothetical situation, answer question no. 9 and 10.

Richa and Anmol are partners sharing profits in the ratio of 3:2 with capitals of ₹2,50,000 and ₹1,50,000 respectively. Interest on capital is agreed @ 6% p.a. Anmol is to be allowed an annual salary of 12,500. During the year ended 31st March 2023, the profits of the year prior to calculation of interest on capital but after charging Anmol’s salary amounted to ₹62,000. A provision of 5% of this profit is to be made in respect of manager’s commission.

Following is their Profit & Loss Appropriation Account

9. The amount to bereflected in blank (1) will be:

a) ₹37,200 b) ₹44,700 c) ₹22,800 d) ₹20,940

View AnswerAns. d) ₹20,940

10. The amount to be reflected in blank (2) will be:

a) ₹62,000. b) ₹74,500. c) ₹71,400. d) ₹70,775.

View AnswerAns. c) ₹71,400.

11. In the absence of an agreement, partners are entitled to:

i) Profit share in capital ratio.

ii) Commission for making additional sale.

iii) Interest on Loan & Advances by them to the firm.

iv) Salary for working extra hours.

v) Interest on Capital.

Choose the correct option:

a) Only i), iv) and v). b) Only ii) and iii). c) Only iii). d) Only i) and iii).

View AnswerAns. c) Only iii).

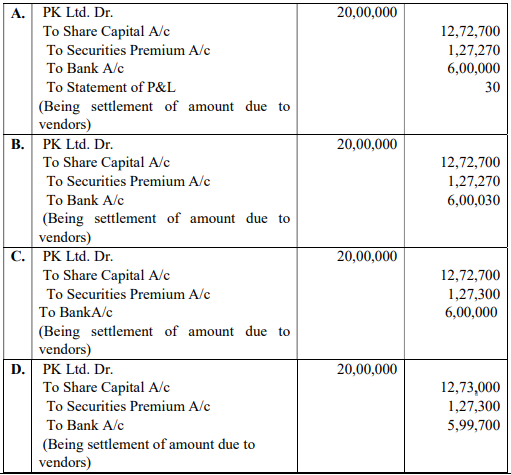

12. Rancho Ltd. took over assets worth ₹ 20,00,000 from PK Ltd. by paying 30% through bank draft and balance by issue of shares of ₹ 100 each at a premium of 10%. The entry to be passed by Rancho Ltd for settlement will be :-

Ans. Option (B)

13. A company forfeited 3,000 shares of ₹10 each, on which only ₹5 per share (including ₹1 premium) has been paid. Out of these few shares were re-issued at a discount of ₹1 per share were and ₹6,000 were transferred to Capital Reserve. How many shares were re-issued?

a) 3,000 shares b) 1,000 shares c) 2,000 shares d) 1,500 shares

View AnswerAns. c) 2,000 shares

14. X and Y are partners in a firm with capital of ₹18,000 and ₹20,000. Z brings ₹10,000 for his share of goodwill and he is required to bring proportionate capital for 1/3rdshare in profits. The capital contribution of Z will be:

a) ₹24,000. b) ₹19,000. c) ₹12,667. d) ₹14,000.

View AnswerAns. a) ₹24,000.

15. A and B are partners. B draws a fixed amount at the end of every quarter. Interest on drawings is charged @15% p.a. At the end of the year interest on B’s drawings amounted to ₹9,000. Drawings of B were:

a) ₹24,000 per quarter.

b) ₹40,000 per quarter

c) ₹30,000 per quarter

d) ₹80,000 per quarter

View AnswerAns. b) ₹40,000 per quarter

OR

Shyam, Gopal & Arjun are partners carrying on garment business. Shyam withdrew ₹ 10,000 in the beginning of each quarter. Gopal, withdrew garments amounting to ₹ 15,000 to distribute it to flood victims, and Arjun withdrew ₹ 20,000 from his capital account. The partnership deed provides for interest on drawings @ 10% p.a. The interest on drawing charged from Shyam, Gopal & Arjun at the end of the year will be

a) Shyam- ₹ 4,800; Gopal- ₹ 1,000; Arjun- ₹ 2,000.

b) Shyam- ₹ 4,800; Gopal- ₹ 1,000; Arjun- ₹ 2,000.

c) Shyam- ₹ 2,500; Gopal- ₹ 750; Arjun- Nil.

d) Shyam- ₹ 4,800; Gopal- Nil; Arjun- Nil.

View AnswerAns. c) Shyam- ₹ 2,500; Gopal- ₹ 750; Arjun- Nil.

16. On the day of dissolution of the firm ‘Roop Brothers’ had partner’s capital amounting to ₹1,50,000 , external liabilities ₹35,000, Cash balance ₹8,000 and P&LA/c(Dr.) ₹7,000. If Realisation expense and loss on Realisation amounted to₹5,000 and ₹25,000 respectively, the amount realised by sale of assets is:

a) ₹1,64,000 b) ₹1,45,000 c) ₹1,57,000 d) ₹1,50,000

View AnswerAns. d) ₹1,50,000

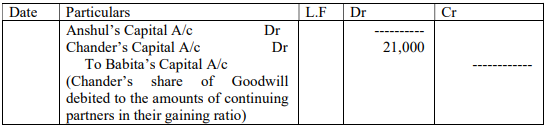

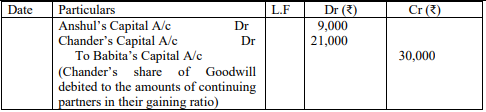

17. Anshul, Babita and Chander were partners in a firm running a successful business of car accessories. They had agreed to share profits and losses in the ratio of 1/2 : 1/3 : 1/6 respectively. After running business successfully and without any disputes for 10 years,Babita decided to retire due to old age and the Anshul and Chander decided to share future profits and losses in the ratio of 3 : 2. The accountant passed the following journal entry for Babita share of goodwill and missed some information. Fill in the missing figures in the following Journal entry and calculate the gaining ratio.

Ans.

Gaining Ratio is 3:7

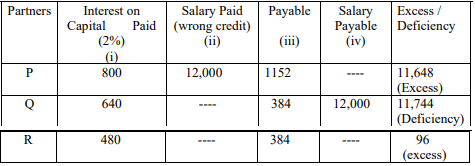

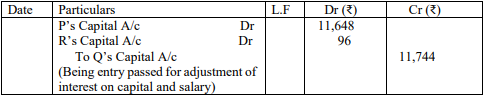

18. P, Q and R were partners with fixed capital of ₹ 40,000, ₹32,000and ₹24,000.After distributing the profit of ₹48,000 for the year ended 31st March 2022 in their agreed ratio of 3 : 1 : 1it was observed that:

(1) Interest on capital was provided at 10% p.a. instead of 8% p.a.

(2) Salary of ₹ 12,000 was credited to P instead of Q.

You are required to pass a single journal entry in the beginning of the next year to rectify the above omissions.

View AnswerAns.

OR

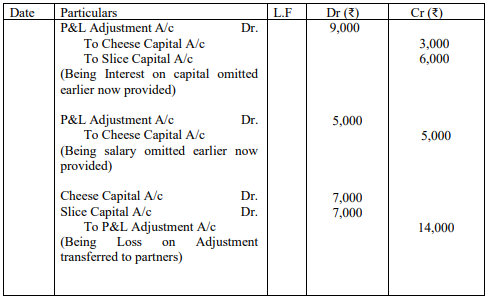

Cheese and Slice are equal partners. Their capitals as on April 01, 2022 were Rs. 50,000 and Rs. 1,00,000 respectively. After the accounts for the financial year ending March 31, 2023 have been prepared, it is observed that interest on capital @ 6% per annum and salary to Cheese @ ₹5,000 per annum, as provided in the partnership deed has not been credited to the partners’ capital accounts before distribution of profits.

You are required to give necessary rectifying entries using P&L adjustment account

View AnswerAns.

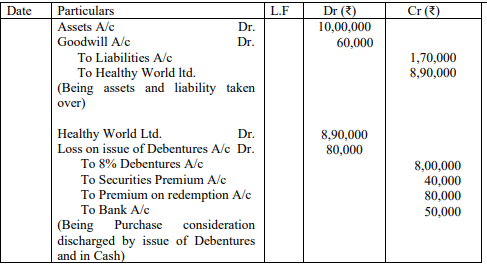

19. Pioneer Fitness Ltd. took over the running business of Healthy World Ltd. having assets of ₹10,00,000 and liabilities of ₹ 1,70,000 by:

a) Issuing 8,000 8% Debentures of ₹ 100 each at 5% premium redeemable after 6 years @ ₹ 110; and

b) Cheque for ₹ 50,000.

Pass the Journal entries in the books of Pioneer Fitness Ltd.

View AnswerAns.

OR

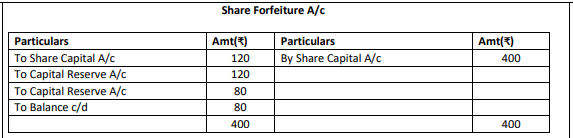

Lilly Ltd. forfeited 100 shares of ₹10 each issued at10% premium (₹8 called up ) on which a shareholder did not pay ₹3 of allotment (including premium) and first call of ₹2. Out of these 60 shares were reissued to Ram as fully paid for ₹8 per share and 20 shares to Suraj as fully paid up @ ₹12 per share at different intervals of time.

Prepare Share Forfeiture account.

View AnswerAns.

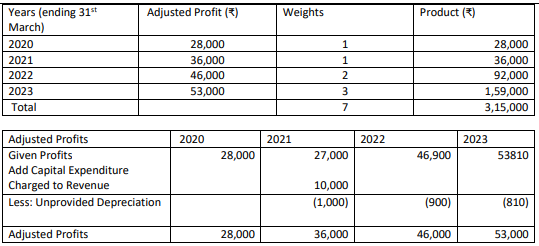

20. Calculate goodwill of a firm on the basis of three years purchases of the Weighted Average Profits of the last four years. The profits of the last four years were:

a) On 1st April, 2020 a major plant repair was undertaken for ₹10,000 which was charged to revenue. The said sum is to be capitalized for goodwill calculation subject to adjustment of depreciation of 10% on reducing balance method.

b) For the purpose of calculating Goodwill the company decided that the years ending 31.03.2020 and 31.03.2021 be weighted as 1 each (being COVID affected) and for year ending 31.03.2022 and 31.03.2023 weights be taken as 2 and 3 respectively.

View AnswerAns.

Weighted Average Profit = 3,15,000/7

=₹45,000

Goodwill = 45,000 × 3 = ₹1,35,000

Notes to Solution

(i) Depreciation of 2021= 10% of 10,000

= 10,000 × 10/100 =₹1,000

(ii) Depreciation of 2022 = 10% of 9000

= 9,000×10/100= ₹900

(iii) Depreciation of 2022 = 10% of 8,100

= ₹8,100

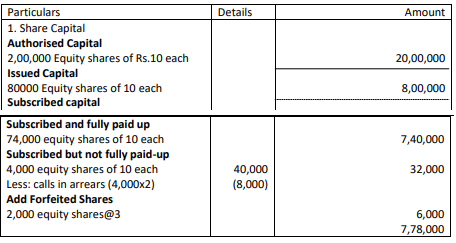

21. Atishyokti Ltd. company was registered with an authorized capital of ₹ 20,00,000 divided into 2,00,000 Equity Shares of ₹ 10 each, payable ₹ 3 on application, ₹ 6 on allotment (including ₹ 1 premium) and balance on call. The company offered 80,000 shares for public subscription. All the money has been duly called and received except allotment and call money on 5,000 shares held by Manish and call money on 4,000 shares held by Alok. Manish’s shares were forfeited and out of these 3,000 shares were re-issued ₹ 9 per share as fully paid up. Show share capital in the books of the company. Also prepare notes to accounts.

View AnswerAns.

Balance Sheet (Extract) as at

Notes to Accounts

Note 1:

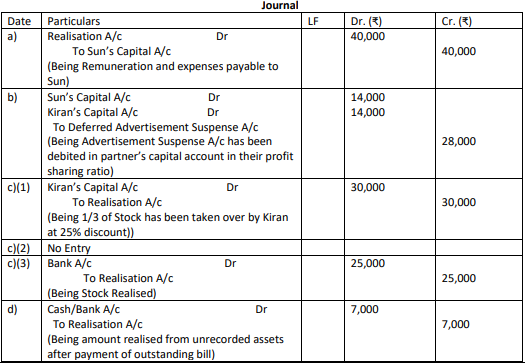

22. Sun and Kiran are partners sharing profits and losses equally. They decided to dissolve their firm. Assets and Liabilities have been transferred to Realisation Account. Pass necessary Journal entries for the following:

a) All partners are agreed that the process of realisation at the time dissolution will be accomplished by Sun for which he will be paid ₹10,000 along with the amount of expense which amounted to 2% of total value realised from the Assets on dissolution. Some assets were sold for Cash at a cumulative Value of ₹12,00,000 and the remaining were taken over by creditors at a valuation of ₹3,00,000.

b) Deferred Advertisement Expenditure A/c appeared in the books at ₹28,000.

c) Out of the Stock of ₹1,20,000; Kiran (a partner) took over 1/3 of the stock at a discount of 25% and 50% of remaining stock was took over by a Creditor of ₹30,000 in full settlement of his claim. Balance amount of stock realized at ₹25,000.

d) An outstanding bill for repairs and renewal of₹3,000 was settled through an unrecorded asset which was valued at ₹10,000. Balance being settled in Cash.

View AnswerAns.

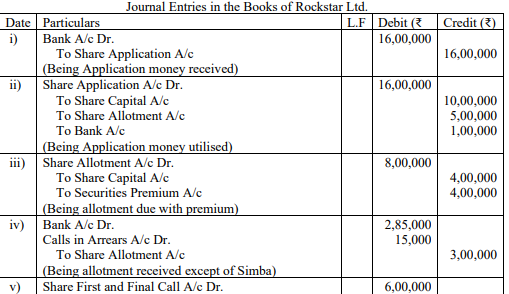

23. The Directors of Rockstar Ltd. invited applications for 2,00,000 Shares of ₹ 10 each, issued at 20% premium. Share was payable as ₹ 5 on application, ₹ 4 (including premium) on allotment and balance on call. Public had applied for 3,20,000 shares out of which applications for 20,000 shares were rejected and remaining were alloted on pro-rata basis.

Simba, an applicant of 15,000 shares failed to pay allotment and call money. His shares were forfeited and out of these 6,000 shares were reissued at a discount of ₹2 per share.

Journalise.

View AnswerAns.

OR

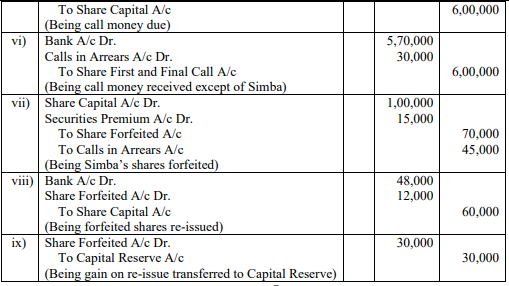

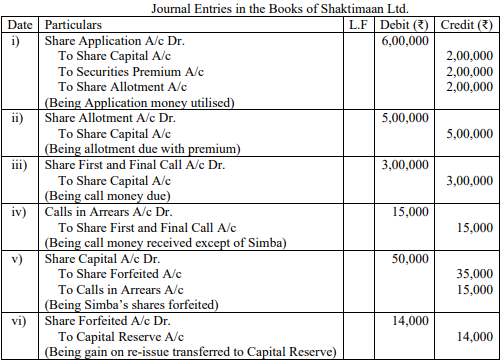

Shaktimaan Ltd. invited applications for issuing 1,00,000 Shares of ₹ 10 each at a premium of ₹2 per share. The amount was payable as₹ 4 on application (including premium); ₹ 5 on Allotment and balance on call. Applications were received shares for 1,80,000 of which Applications for 30,000 shares were rejected and remaining applicants were allotted on pro-rata basis.

Manthan, holding 5,000 shares failed to pay call money and his shares were forfeited. Out of these 2,000 shares were re-issued at premium of ₹ 3 per share. Prepare Cash Book and pass necessary entries.

View AnswerAns.

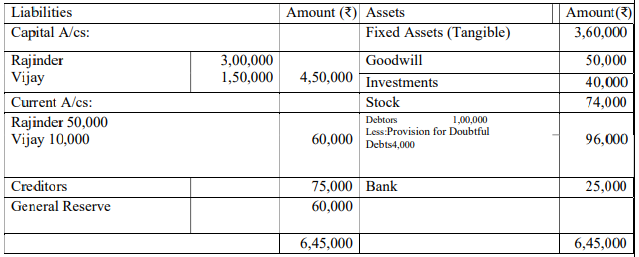

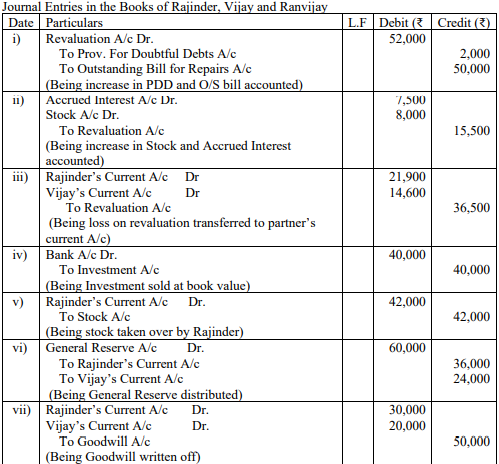

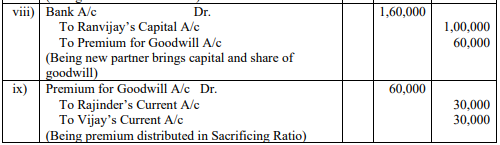

24. Rajinder and Vijay were partners in a firm sharing profits in the ratio 3:2. On 31st March 2023 their balance sheet was as follows:

With an aim to expand business it is decided to admit Ranvijay as a partner on 1st April 2023 on the following terms:

a) Provision for doubtful debts is to be increased to 6% of debtors.

b) An outstanding bill for repairs ₹ 50,000 to be accounted in the books

c) An unaccounted interest accrued of ₹ 7500 be provided for .

d) Investment were sold at book value.

e) Half of stock was taken by Rajinder at ₹42,000 and remaining stock was also to be revalued at the same rate.

f) New profit-sharing ratio of partners will be 5:3:2.

g) Ranvijay will bring ₹ 1,00,000 as capital and his share of goodwill which was valued at twice the average profit of the last three years ended 31st March 2023, 2022 and 2021 were ₹ 1,50,000, ₹ 1,30,000 and ₹ 1,70,000 respectively.

Pass necessary journal entries.

View AnswerAns.

OR

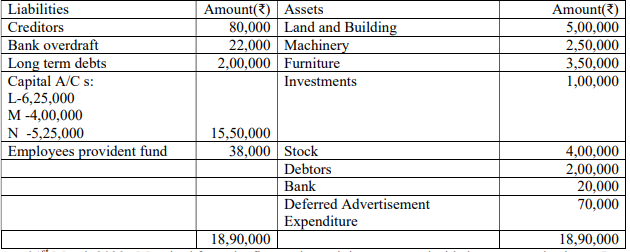

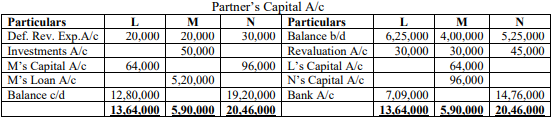

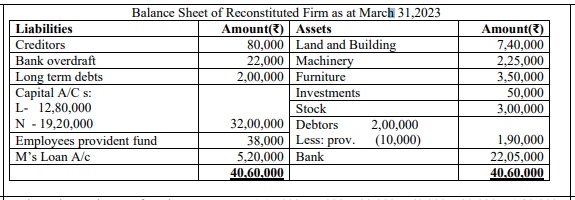

L, M and N were partners in a firm sharing profit & losses in the ratio of 2:2:3 . On 31st March 2023, their Balance Sheet was as follows:

On 31st March 2023 , M retired from the firm and remaining partners decided to carry on business. It was decided to revalue assets and liabilities as under :

a) Land and Building be appreciated by₹ 2,40,000 and Machinery be depreciated 10%.

b) 50% of investments were taken by the retiring partner at book value.

c) Provision for doubtful debts was to be made at5% on debtors.

d) Stock will be valued at market price which is ₹1,00,000 less than the book value.

e) Goodwill of the firm be valued at ₹5,60,000. L and N decided to share future profits and losses in the ratio of 2:3.

f) The total capital of the new firm will be ₹32,00,000 which will be in proportion of profit – sharing ratio of L and N.

g) Gain on revaluation account amounted to ₹1,05,000.

Prepare Partner’s Capital accounts and Balance sheet of firm after M’s retirement.

View AnswerAns.

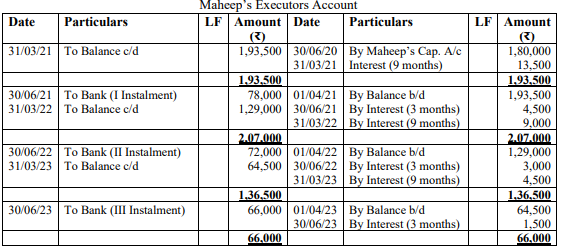

25. Sandeep, Maheep and Amandeep were partners in a firm sharing profits in the ratio of 2: 2: 1. The firm closes its books on 31st March every year. On 30th June, 2020 Maheep died. The partnership deed provided that on the death of a partner his executors will be entitled to the following:

a) Balance in his capital account which amounted to ₹1,15,000and interest on capital till date of death which amounted to ₹5,000.

b) His share in the profits of the firm till the date of his death amounted to ₹20,000.

c) His share in the goodwill of the firm. The goodwill of the firm on Maheep’s death was valued at ₹1,50,000.

d) Loan to Maheep amounted ₹ 20,000.

It was agreed that the amount will be paid to his executor in three equal yearly instalments with interest @10% p.a. The first instalment was to be paid on 30.06.2021.

Calculate the amount to be transferred to Maheep’s executors Account and prepare the executor’s account till it is finally settled.

View AnswerAns.

Maheep dues to be transferred to executors = 1,15,000 + 5,000 + 20,000 + 60,000 – 20,000 = 1,80,000

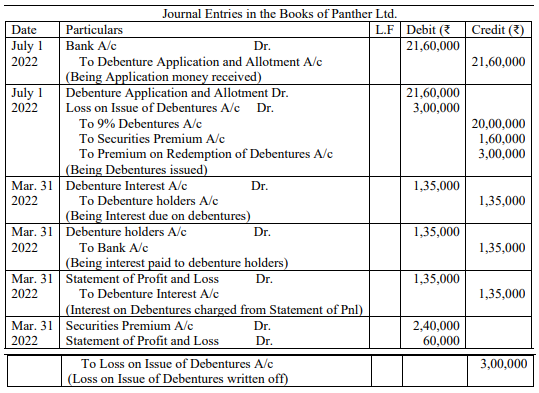

26. On July 01, 2022, Panther Ltd. issued 20,000, 9% Debentures of ₹ 100 each at 8% premium and redeemable at a premium of 15% in four equal instalments starting from the end of the third year. The balance in Securities Premium on the date of issue of debentures was ₹ 80,000. Interest on debentures was to be paid on March 31 every year.

Pass Journal entries for the financial year 2022-23. Also prepare Loss on Issue of Debentures account.

View AnswerAns.

PART B

Option – I

(Analysis of Financial Statements)

27. ‘Freedom to Choose of method of depreciation’ refers to which limitation of financial statement analysis.

a) Historical analysis.

b) Qualitative aspect ignored.

c) Not free from bias.

d) Ignore Price level Changes.

View AnswerAns. c) Not free from bias.

OR .

………… is included in current assets while preparing balance sheet as per revised Schedule III but excluded from current assets while calculating Current Ratio

a) Debtors.

b) Cash and Cash Equivalent.

c) Loose tools and Stores and spares.

d) Prepaid Expense.

View AnswerAns. c) Loose tools and Stores and spares.

28. Debt-Equity Ratio of Dhamaka Ltd is 3 : 1. Which of the following will result in decrease in this ratio?

a) Issue of Debentures for Cash of ₹2,00,000.

b) Issue of Debentures of ₹3,00,000 to Vendors from whom Machinery was purchased.

c) Goods purchased on Credit of ₹1,00,000.

d) Issue of Equity Shares of ₹2,00,000.

View AnswerAns. d) Issue of Equity Shares

29. Statement I: – Sale of Marketable Securities will result in no flow of Cash.

Statement II: – Debentures issued as collateral security will result in inflow of cash

A. Both Statements are correct.

B. Both Statements are incorrect.

C. Statement I is correct and Statement II is incorrect.

D. Statement I is incorrect and Statement I is correct.

View AnswerAns. C. Statement I is correct and Statement II is incorrect.

OR

What will be the effect of issue of Bonus shares on Cash Flow Statement?

A. No effect

B. Inflow in Financing Activity

C. Inflow in Operating activity

D. Inflow in Investing Activity

View AnswerAns. A. No effect

30. Aditya Sunrise Ltd. provides you the following information:

Additional Information:

1. Equity Share Capital raised during the year ₹3,00,000;

2. 10% Bank Loan was repaid on 01.04.2022.

3. Dividend received during the year was ₹20,000.

4. Dividend Proposed for the year 2021-22 was ₹50,000 but only ₹20,000 was approved by the Shareholders.

Find out the cash flow from Financing Activities.

a) ₹ 1,50,000 b) ₹ 2,00,000 c) ₹ 1,70,000 d) ₹ 1,80,000

View AnswerAns. d) ₹ 1,80,000

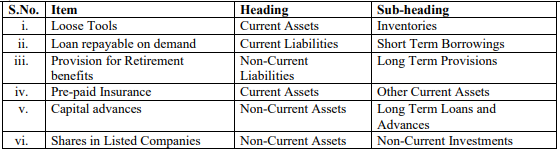

31. Classify the following items under Major heads and Sub heads (If any) in the balance sheet of a Company as per schedule III of the Companies Act 2013.

Ans.

32. a) A company had a liquid ratio of 1.5 and current ratio of 2 and inventory turnover ratio 6 times. It had total current assets of ₹8,00,000. Find out annual sales if goods are sold at 25% profit on cost.

b) Calculate debt to capital employed ratio from the following information.

Shareholder funds ₹ 15,00,000

8% Debenture ₹ 7,50,000

Current liabilities ₹ 2,50,000

Non -current Assets ₹ 17,50,000

Current Assets ₹7,50,000

View AnswerAns. (a). Current Ratio = Current Assets / Current Liabilities

2 = 8,00,000 / Current Liabilities

So, Current Liabilities = ₹ 4,00,000

Liquid Ratio = Liquid Assets / Current Liabilities

1.5 = Liquid Assets / 4,00,000

So, Liquid Assets = ₹ 6,00,000

Inventory = Current Assets – Liquid Assets

Inventory = 8,00,000 – 6,00,000 = ₹ 2,00,000

Inventory Turnover Ratio = Cost of Revenue From Operations / Average Inventory

6 = Cost of Revenue from Operations / 2,00,000

Cost of Revenue from Operations = ₹ 12,00,000

Gross Profit = 25% of Cost i.e ₹ 3,00,000

Revenue From Operations = Cost of Revenue from Operations + Gross Profit = 12,00,000 + 3,00,000

Revenue From Operations = ₹ 15,00,000

(a) Debt to Capital employed ratio = Debt / Capital Employed

Debt to Capital employed ratio = 7,50,000 / (7,50,000 + 15,00,000) = 7,50,000 / 22,50,000

Debt to Capital employed ratio = 1/3 = 0.33 : 1

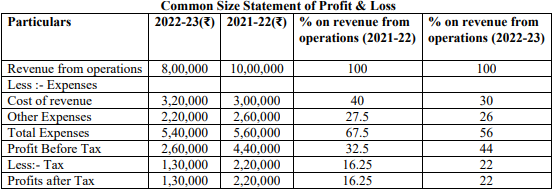

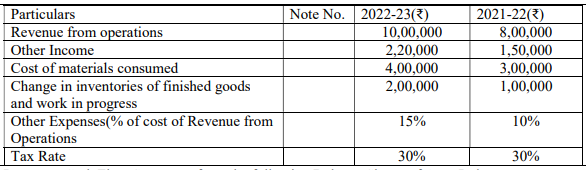

33. From the information extracted from the statement of Profit & Loss of Zee Ltd for the year ended 31st March 2022 and 31st March 2023, prepare a common size statement of profit & loss:

Ans.

OR

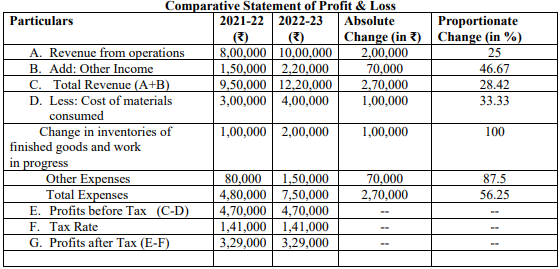

From the following information, prepare comparative statement of Profit & Loss

Ans.

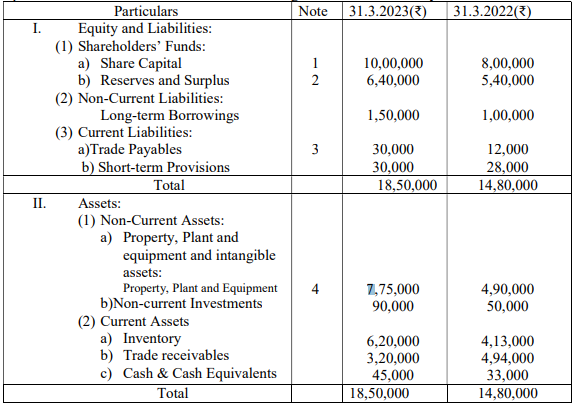

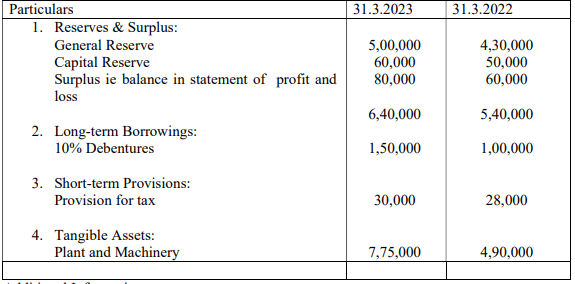

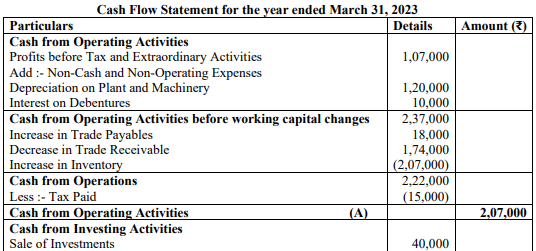

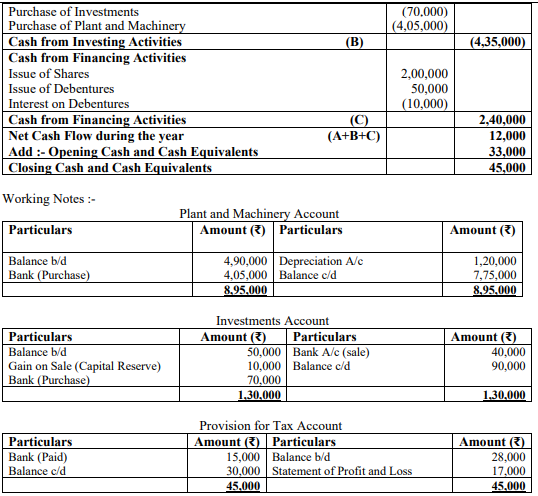

34. Prepare a Cash Flow Statement from the following Balance Sheets of Arya Ltd.:

Notes to Accounts:

Additional Information:

1. Tax provided during the year is ₹17,000.

2. Depreciation charged on plant and Machinery during the year amounted to ₹1,20,000.

3. Non-current Investments costing ₹ 30,000 were sold for ₹ 40,000 during the year. Gain on sale of Investments was credited to Capital Reserve.

4. Additional Debentures were issued on 31.03.2023

View AnswerAns.

Net Profits after Tax and Extraordinary Items = 20,000

+ Transfer to General Reserve = 70,000

+ Provision for Tax = 17,000

= Net Profits before Tax and Extraordinary Items = 1,07,000

PART B

Option – II

(Computerised Accounting)

27. Which formulae would result in TRUE if C3 is less than 14 and D4 is less than 200? (a)=AND(C3>14,D4>20)

(b)=AND(C3>14,C4<200)

(c)=AND(C3>14, D4<20)

(d)=AND(C3<14,D4,200)

View AnswerAns. (d)=AND(C3<14,D4,200)

28. When navigating in a work book, which command is used to move to the beginning of the current row?

(a) [Ctrl]+[Home]

(b) [Page Up]

(c) [Home]

(d) [Ctrl]+[Backspace] View Answer

Ans. (c) [Home]

Or

Which function results can be displayed in Auto Calculate?

(a) SUM and AVERAGE

(b) MAX and LOOK

(c) LABEL and AVERAGE

(d) MIN and BLANK

View AnswerAns. (a) SUM and AVERAGE

29. What category of functions is used in this formula:=PMT(D11/15,D12,D 12,5)

(a) Logical (b) Financial (c) Payment (d) Statistical

View AnswerAns. (b) Financial

30. The syntax of PMT Function is _____________

(a) PMT(rate,pv,nper, [fv],[type])

(b) PMT(rate,nper,pv,[fv],[type])

(c) PMT(rate,pv,nper,[type],[fv])

(d) PMT(rate,nper,pv,[type],[fv])

View AnswerAns. (a) PMT(rate,pv,nper, [fv],[type])

Or

In Excel, the chart tools provide three different options , and for formatting.

(a) Layout, Format, Data Maker

(b) Design, Layout, Format

(c) Format, Layout, Label

(d) Design, Data Maker, Layout

View AnswerAns. (b) Design, Layout, Format

31. State any three requirements which should be considered before making an investing decision to choose between ‘Desktop database’ or ‘Server database’.

View AnswerAns. The points to be considered before making investment in a database: (any three)

(i) What all data is to be stored in the database?

(ii) Who will capture or modify the data, and how frequently the data will be modified?

(iii) Who will be using the database, and what all tasks will they perform?

(iv) Will the database (backend) be used by any other frontend application?

(v) Will access to database be given over LAN/ Internet, and for what purposes?

(vi) What level of hardware and operating system is available?

32. ‘Accounting Vouchers used for entry in Tally software’

Define any three types of vouchers which form the basis of entry in Tally software.

View AnswerAns. Types of Accounting Vouchers

(i) Contra Vouchers

(ii) Payments Vouchers

(iii) Receipt Vouchers

33. Explain the use of ‘Conditional Formatting’.

View AnswerAns. Uses of conditional formatting:

(i) It helps in making needed information highlighted.

(ii) It changes the appearance of cells ranges.

(iii) Color scale may be used to highlight cells.

(iv) useful in making decision making.

Or

State the features of Computerized Accounting system.

View AnswerAns. Features of computerized accounting system:

(i) Simple and integrated.

(ii) Transparency and control.

(iii) Accuracy and speed.

(iv) Scalability.

(v) Reliability.

34. Describe two basic methods of charging depreciation. Differentiate between both of them.

View AnswerAns. Two basic methods of charging depreciation are:

Straight line method: This method calculates fixed amount of depreciation every year which is calculated keeping in view the useful life of assets and its salvage value at the end of its useful life. Written down value method: This method uses current book value of the asset for computing the amount of depreciation for the next period. It is also known as declining balance method.

Differences:

1. Equal amount of depreciation is charged in straight line method. Amount of depreciation goes on decreasing every year in written down value method.

2. Depreciation is charged on original cost in straight line method. The amount is calculated on the book value every year.

3. In straight line method the value of asset can come to zero but in written down value method this can never be zero.

4. Generally rate of depreciation is low in case of straight line method but it is kept high in case of written down value method.

5. It is suitable for assets in which repair charges are less and the possibility of obsolescence is less. It is suitable for the assets which become obsolete due to changes in technology.