Money and Credit

1. What is a barter system?

View AnswerAns. Barter system is a condition in which goods are exchanged without the use of money.

2. Why is money called a medium of exchange? Who supervises the functioning of formal sources of loan?

OR

How does money act as medium of exchange?

View AnswerAns. Money acts as an intermediate in the exchange process and eliminates the need for double coincidence of wants. As money acts as intermediate, it is also called medium of exchange.

3. Recognise the situation when both the parties in a barter economy have to agree to sell and buy each other’s commodities. What is it called?

View AnswerAns. This is known as double coincidence of wants.

4. What is meant by double coincidence of wants?

View AnswerAns. Both parties, the seller and the buyer have to agree to sell and buy each other commodities. Goods are directly exchanged without the use of money.

5. How does money eliminate the need for double coincidence of wants?

View AnswerAns. If we have money in our pocket we can purchase anything at any time as we wish.

6. Why one cannot refuse a payment made in rupees in India?

View AnswerAns. One cannot refuse a payment made in rupees because it is accepted as a medium of exchange. The currency is authorized by the government of India.

7. Why do banks maintain cash reserve?

View AnswerAns. Banks maintain cash reserve to arrange for daily withdrawals by depositors.

8. How do the deposits with banks become their source of income?

View AnswerAns. Banks charge higher interest rate on loans than what they offer on deposits. The difference of interest is the main source of income of banks.

9. Highlight the inherent problem in double coincidence of wants.

View AnswerAns. The inherent problem in double coincidence of wants is that both parties have to agree to sell and buy each other’s commodities.

10. How does the use of money make it easier to exchange things? Give an example

View AnswerAns. A person holding money can easily exchange it for any commodity or service that he or she might want. Example: The shoe manufacturer will first exchange shoes that he has produced for money and then exchange the money for wheat.

11. Why is money called a medium of exchange?

View AnswerAns. Money acts as an intermediate in the exchange process.

12. Explain the meaning of currency?

View AnswerAns. Currency is modern forms of money that includes paper notes and coins and accepted as a medium of exchange. It is issued by the Reserve Bank of India on behalf of the central government.

13. How does the Reserve Bank of India supervise the functioning of banks? Why is this necessary?

View AnswerAns. Reserve Bank of India (RBI) supervises the banks in the following ways:

(i) It monitors the balance kept by banks for day-to-day transactions.

(ii) It checks that the banks give loans not just to profit-making businesses and traders but also to small borrowers.

(iii) Periodically, banks have to give details about lenders, borrowers and interest rate to RBI. It is necessary for securing public welfare. It avoids the bank to run the business with profit motive only. It also keeps a check on interest rate of credit facilities provided by bank. RBI makes sure that the loans from the banks are affordable and cheap.

14. How do banks mediate between those who are in need of money and those who have surplus money?

OR

How do banks mediate between those who have surplus money and those who need money?

View AnswerAns. (i) Banks keep small proportion of their deposit as cash with themselves.

(ii) Major portion of deposit is used for extending loans.

(iii) The banks mediate between depositors and borrowers in this way.

(iv) They charge high rate of interest on loans than what they offer on deposits.

15. How will money be easily exchanged itself for goods or services? Give example to explain

View AnswerAns. Money acts as a medium to exchange itself for goods and services: A person holding money can easily exchange it for any commodity or service that he or she might want. Everyone prefers to receive payments in money and exchange the money for things they want. For example, a shoemaker wants to sell shoes in the market and buy wheat. The shoemaker will first exchange shoes for money and then exchange the money for wheat. If the shoemaker had to directly exchange shoes for wheat without the use of money, he would have to look for a wheat growing farmer who not only wants to sell wheat but also wants to buy the shoe in exchange. Both the parties have to agree to sell and buy each other’s commodities. This process is very difficult, time consuming and unhealthy.

16. What are the modern forms of money? Why is the ‘rupee’ widely accepted as a medium of exchange? Explain two reasons.

OR

“The rupee is widely accepted as a medium of exchange.” Explain.

View AnswerAns. The modern forms of money are listed below:

(i) Paper currency (ii) Coins (iii) Demand deposits (iv) Cheques

The rupee is accepted as a medium of exchange in the following ways:

(i) The currency is authorised by the government of the country.

(ii) In India, the Reserve Bank of India issues, currency notes on behalf of the central government.

(iii) The law legalises the use of rupee as a medium of payment that cannot be refused in setting transactions in India.

(iv) No individual in India can legally refuse a payment made in rupees. Hence, the rupee is widely accepted as a medium of exchange.

17. How is money transferred from one bank account to another bank account? Explain with an example.

View AnswerAns. Money is transferred from one bank account to another bank account: If a person has to make a payment to his or her friend and writes a cheque for a specific amount, this means that the person instructs his bank to pay this amount to his friend. His friend takes this cheque and deposits it in his account in the bank. This said amount is transferred from one bank account to another bank account.

18. Why is money transaction system better than barter system? Explain with examples.

View AnswerAns. (i) Transaction system is better than barter system because double coincidence of wants creates problem.

(ii) For example, shoe manufacturer wants to sell shoes in the market and wants to buy wheat. For this, he would look for a wheat growing farmer who would exchange his wheat with the shoes.

(iii) In barter system, goods are exchanged without the use of money.

(iv) In contrast, in an economy where money is in use; money by providing the crucial intermediate step eliminates the need for double coincidence of wants.

19. “Focuses of currency have undergone several changes since early times.” Elucidate.

View AnswerAns. (i) Before the introduction of coins, a variety of objects were used as money.

(ii) In the very early ages, Indians used grains and cattle as money.

(iii) Thereafter, came the use of metallic coins – gold, silver, copper coins.

(iv) Modern forms of money include currency like paper notes and coins.

(v) It is accepted as a medium of exchanges because the currency is authorized by the country’s government.

(vi) It is not made of precious metal; it is without any use of its own.

20. Explain any three loan activities of banks in India.

View AnswerAns. (i) Banks keep only a small proportion of their deposits as cash with themselves, as a provision to pay the depositors who might come to withdraw from the bank on any given day.

(ii) They use their major portion of the deposits to extend loans, mediate between those people who have surplus funds (depositors) and those who are in need of those funds (the borrowers).

(iii) They charge higher rate of interest on the loans than what they offer on deposits. The difference between what is charged from borrowers and what is paid to depositors is their main source of income.

21. How far is it correct to say that money in your pocket cannot buy the basic needs to live well? Explain.

View AnswerAns. (i) Income by itself is not a completely adequate indicator.

(ii) Money cannot buy you a pollution-free environment.

(iii) Money may also not be able to protect you from infectious diseases.

Therefore, the whole community needs to take preventive steps, i.e.

(i) Collective security for the whole society.

(ii) Public facilities such as schools.

(iii) Public Distribution System in some states.

(iv) All can only be done collectively and not individually.

22. How do demand deposit have the essential features of money? Explain.

View AnswerAns. The demand deposits have the essential features of money because:

(i) Banks accept the deposits and also pay an amount as interest on the deposits.

(ii) People also have the provision to withdraw the money as and when they require.

(iii) People’s money is safe with the banks and it earns an amount as interest.

23. “Deposits with the banks are beneficial to the depositors as well as to the nation”. Examine the statement.

View AnswerAns. Banks play an important role in an economy of a country:

(i) They give interest on the money deposited by the people. Thus, they add to the income of the family. Many families survive on the bank interest.

(ii) Banks mediate between those who have surplus money and those who need money.

(iii) Banks provide cheap loans to a large number of people. They promote agriculture by providing loans to the farmers for bringing new farm implements and make better arrangements for the irrigation of their fields.

(iv) Banks boost the industry also by providing cheap loans to industrialists.

(v) They are the backbone of the country’s trade.

(vi) They employ a large number of people and as such they solve the problem of unemployment to a great extent.

24. Why is modern currency accepted as a medium of exchange without any use of its own? Find out the reason.

View AnswerAns. Modern currency is accepted as a medium of exchange without any use of its own because:

(i) Modern currency is authorised by the government of a country.

(ii) In India, the Reserve Bank of India issues all currency notes on behalf of the Central Government.

(iii) No other individual or organisation is allowed to issue currency.

(iv) The law legalises the use of rupee as a medium of payment that cannot be refused in settling transactions in India.

(v) No individual in India can legally refuse a payment made in rupees

25. What are demand deposits? Explain any three features of it?

OR

Which type of deposits with the banks are called demand deposits? State some important features of demand deposits.

View AnswerAns. People save their money in banks by opening an account. The deposits in the bank accounts can be withdrawn on demand, so these deposits are called demand deposits.

(i) Banks accept the deposits and also pay an interest rate on the deposits. In this way people’s money is safe with the banks and it earns an interest.

(ii) The facility of cheques against demand deposits makes it possible to directly settle payments without the use of cash. Since demand deposits are accepted widely as a means of payment, along with currency, they constitute money in the modern economy.

(iii) It is authorised by the government of the country.

(iv) Its demand and supply can be controlled RBI.

(v) In India, the law legalises the use of rupee as a medium of payment that cannot be refused in settling transaction in the country. No individual can legally refuse a payment made in rupees.

26. How are deposits with the bank beneficial for individual as well as for the nation? Explain with examples.

View AnswerAns. The deposits with banks are beneficial for individual as well as for nation:

(i) Banks accept deposit and also pay an amount as interest and in this way people earn money.

(ii) People’s money is safe with banks.

(iii) It is easy for individuals to get credit who have savings and current account in the banks.

(iv) Poor people who are engaged in production need credit.

(v) Credit provided by the banks for government projects help in development of the nation.

27. Why is it necessary for the banks and cooperative societies to increase their lending facilities in rural areas? Explain.

OR

Why should the banks and cooperative societies provide more loan facilities to the rural households in India? Give four reasons.

View AnswerAns. (i) India is an agricultural country so the people in rural areas deserve a special attention. Hence, the banks and cooperative societies should help the needy people in rural areas.

(ii) Mostly, the people in rural areas are illiterate and hence they can be easily cheated by the moneylenders.

(iii) Most loans from informal lenders carry a very high interest rate and do little to increase the income of the borrowers. Hence, it is necessary that banks and cooperatives increase their lending particularly in rural areas, so that the dependence on informal sources of credit reduces.

(iv) Only the banks and cooperative societies can provide loans to the rural household at cheap rates which can easily save them from the clutches of the moneylenders.

(v) Most of the people in urban areas depend upon the rural people for their food requirements, etc. and, their welfare is most important. Hence, the banks and cooperative societies should provide more facilities to the rural households in the matter of advancing loan.

28. How does the use of money make exchange of things easier? Explain with examples.

View AnswerAns. (i) Money means wealth around which the whole economic activities of every country move. It acts as an intermediate in the exchange process and therefore, called a medium of exchange.

(ii) In our day to day transactions, goods are being bought and sold with the use of money. At times we do exchange services with money.

(iii) Use of money has made things easier to exchange as we can exchange it for any commodity we need.

(iv) The transactions are made in money because a person holding money can easily exchange it for any commodity or service that he or she wants.

(v) Thus, the main function of money in an economic system is to facilitate the exchange of goods and services. Without exchange of money nobody can fulfil his all needs and requirements

29. Why do banks ask for collateral while giving loans?

View AnswerAns. Banks use collateral as a guarantee until the loan is repaid

30. What is meant by term of credit? What does it include?

View AnswerAns. Terms of credit are the requirements need to be satisfied for any credit arrangements. It includes interest rate, collateral, documentation and mode of repayment. However, the terms of credit vary depending upon the nature of lender, borrower and loan

31. Why do lenders ask for collateral while lending? Give any three reasons.

OR

Why do lenders ask for collateral while lending? Explain.

View AnswerAns. The lenders ask for collateral while lending because collateral, means security, is an assets that the borrower owns (such as land, building, vehicle, livestocks, deposits with banks) and uses this as a guarantee to a lender until the loan is repaid. If the borrower fails to repay the loan, the lender has the right to sell the assets or collateral to obtain payment.

Thus, every loan agreement specifies an interest rate which the borrower must pay to the lender along with the repayment of the principal.

32. Why is credit a crucial element in the economic development?

View AnswerAns. Credit is a crucial element in economic development of a country because:

(i) It helps to meet the ongoing expenses of production

(ii) It helps in increasing earnings

(iii) It helps in completing production in time.

33. How do banks play an important role in the economy of India? Explain.

OR

“Bank plays an important role in the economic development of the country.” Support the statement with examples.

View AnswerAns. Banks play an important role in developing the economy of India:

(i) They keep money of the people in its safe custody.

(ii) They give interest on the deposited money to the people.

(iii) They mediate between those who have surplus money and those who are in need of money.

(iv) They provide loan to large number of people at low interest rate.

(v) They promote agricultural and industrial sector by providing loans.

(vi) They also provide funds to different organisations.

34. Describe the vital and positive role of credit with examples.

OR

What is credit? How does credit play a vital and positive role? Explain with an example.

View AnswerAns. Credit refers to an agreement in which the lender supplies the borrower with money, goods or services in return for the promise of future payment. Credit plays a vital and positive role as:

(i) Credit helps people from all walks of life in setting up their business, increase their income and support their families.

(ii) To some people loan helps a lot in constructing their houses and get relief from monthly rent.

(iii) To others it helps a lot in raising their standards.

(iv) Example: It is festival season two months from now and the shoe manufacturer, Salim, has received an order from a large trader in town for 3,000 pairs of shoes to be delivered in a month time. To complete production on time, Salim has to hire a few more workers for stitching and pasting work. He has to purchase the raw materials. To meet these expenses, Salim obtains loans from two sources. First, he asks the leather supplier to supply leather now and promises to pay him later. Second, he obtains loan in cash from the large trader as advance payment for 1000 pairs of shoes with a promise to deliver the whole order by the end of the month. At the end of the month, Salim is able to deliver the order, make a good profit, and repay the money that he had borrowed.

The credit helps him and now he is able to increase his earnings.

35. “Credit sometimes pushes the borrower into a situation from which recovery is very painful.” Support the statement with examples.

View AnswerAns. In rural areas, the main demand for credit is for crop production. Crop production involves considerable costs on seeds, fertilisers, pesticides, water, electricity, repair of equipment, etc. There is a minimum stretch of three to four months between the time when the farmers buy these inputs and when they sell the crop. Farmers usually take crop loans at the beginning of the season and repay the loan after harvest. Repayment of the loan is crucially dependent on the income from farming.

If the failure of the crop made loan repayment impossible then farmers had to sell part of the land to repay the loan. Credit, instead of helping those farmers to improve their earnings, left them worse off and they came into the debt-trap. In this case credit pushes the borrower into a situation from which recovery is very painful.

In one situation credit helps to increase earnings and therefore the person is better off than before. In another situation, because of the crop failure, credit pushes the person into debt trap. To repay the loan farmers have to sell a portion of their land. They are now clearly much worse off than before. Whether credit would be useful or not, therefore, depends on the risks in the situation and whether there is some support in case of loss.

Thus, through the above situation or example, we can easily say that credit sometimes pushes the borrower into a situation from which recovery is very painful.

36. Prove with an argument that there is a great need to expand formal sources of credit in rural India.

View AnswerAns. To expand formal sources of credit in rural India, dependence on informal sources of credit has to be reduced.

37. Why are most of the poor households deprived from the formal sector of loans?

View AnswerAns. They are deprived from the formal sector of loans because of:

(i) Lack of collateral.

(ii) They are illiterate.

(iii) They cannot fulfil the formalities of the formal sector of loans.

38. Why is the supervision of the functioning of formal sources of loans necessary?

View AnswerAns. It is necessary because banks have to submit information to the RBI on how much they are lending, to whom they are lending and what interest rate, etc.

39. Give any two examples of informal sector of credit.

View AnswerAns. Two examples of informal sector of credit are: (i) moneylenders, (ii)traders, (iii) employers, (iv) relatives, (v) friends.

40. Explain the importance of formal sector loans in India.

View AnswerAns. Importance of formal sector loans in India:

(i) They provide loans at a fixed rates and terms.

(ii) They give loans not just to profit making business and traders but also to small cultivators, small-scale industries too small borrowers, etc.

41. Explain the reason for necessity of supervision by the Reserve Bank of India of formal source of loans.

View AnswerAns. The Reserve Bank of India supervises the functioning of formal sources of loans because banks are giving loans to small cultivators, small scale industries, to small borrowers or not only to profit-making businesses and traders.

42. Formal credit meets only about half of the total credit needs of the rural people. Where does the other half come from?

View AnswerAns. (i) Compared to formal lenders, most of the informal lenders charge much higher interest rates on loans like 3% to 5% per month, i.e., 36% a year.

(ii) Besides the high interest rate, informal lenders impose various other tough conditions. For example, they make the farmers promise to sell the crop to him at a low price. There is no such condition in formal sector.

(iii) Loans taken by poor people from informal lenders sometimes, lead them to debt trap because of high interest rate.

(iv) The formal sources of credit in India still meets only about half of the total credit needs of the rural people.

43. Dhananjay is a government employee and belongs to a rich household, whereas Raju is a construction worker and comes from a poor rural household. Both are in need and wish to take loan. Create a list of arguments explaining who between the two would successfully be able to arrange money from a formal source. Why?

View AnswerAns. Dhananjay will be able to get loan from a formal source.

Arguments:

Banks are not present everywhere in rural India. Even when they are present, getting a loan from a bank is much more difficult than taking a loan from informal sources. Bank loans require proper documents and collateral. Absence of collateral is one of the major reasons which prevents the poor from getting bank loans. Informal lenders such as moneylenders, on the other hand, know the borrowers personally and hence, are often willing to give a loan without collateral.

44. In what ways does the Reserve Bank of India supervise the functioning of banks? Why is this necessary?

OR

How does the Reserve Bank of India supervise the functioning of banks? Why is this necessary?

View AnswerAns. RBI sees that the banks maintain the minimum cash balance or not. It monitors that the loan is not just given to the profit–making businesses and traders but also to the small borrower. It asks the banks to submit information like how much they are lending, to whom they are lending and at what rate of interest, etc.

45. Why is cheap and affordable credit important for the country’s development? Explain any three reasons.

View AnswerAns. Cheap and affordable credit is important for the country’s development because of the following reasons:

(i) This would lead to higher incomes and many people could then borrow cheaply for a variety of needs.

(ii) With the help of cheap credit they could grow crops, do business, set up small scale industries which will generate employment and help in country’s development.

(iii) They could set up new industries or trade in goods. It will lead to the country’s development.

46. Describe the importance of formal sources of credit in the economic development.

View AnswerAns. Importance of formal sources of credit in the economic development:

(i) This would lead to higher incomes and many people could then borrow cheaply for a variety of needs.

(ii) They could grow crops, do business, set up small scale industries, etc.

(iii) They could set up new industries or trade. All these lead to the country’s development.

47. Describe the bad effects of informal sources of credit on borrowers.

View AnswerAns. The bad effects of informal sources of credit on borrowers:

(i) Most of the informal lenders charge a much higher interest on loans. Thus the cost to the borrower of the informal loans is much higher.

(ii) There is no boundaries or restrictions.

(iii) Higher cost of borrowing means a larger part of earning of the borrowers is used to repay the loan and they have less income left for themselves.

(iv) The high rate of interest of borrowing can mean that the amount to be repaid is greater than the income of the borrower and it can lead to increasing debt and debt-trap.

(v) People who might wish to start an enterprise by borrowing may not do so because of the high cost of borrowing.

48. Explain any three reasons for the banks and cooperative societies to increase their lending facilities in rural areas.

View AnswerAns. The three reasons for the banks and cooperative societies to increase their lending facilities in rural areas are:

(i) India is an agricultural country so the people in rural areas deserve a special attention, hence, the banks and cooperative society should help the needy people in rural areas.

(ii) Mostly the people in rural areas are illiterate and hence they can be easily cheated by the money lenders.

(iii) Only the banks and cooperative societies can provide loans to the rural household at cheap rates which can easily save them from the clutches of the money lenders.

49. Why do we need to expand formal sources of credit in India? Explain.

View AnswerAns. Expand formal sources:

(i) To save people from the exploitation of Informal sector.

(ii) Formal charge a low interest on loans.

(iii) To save from debt trap.

(iv) It provides cheap and affordable credit.

(v) RBI also supervises the formal sector credit through various rules and regulations which ensures that banks give loans to small cultivators, small borrowers, etc. and not just to profit making business and traders.

50. Why do banks and cooperative societies need to lend more? Explain.

View AnswerAns. Banks and cooperative societies need to lend more:

(i) This would lead to higher incomes. (ii) People could borrow cheaply for a variety of needs.

(iii) They could grow crops and set up small-scale industries etc.

(iv) Cheap and affordable credit is crucial for the country’s development.

(v) To save and reduce the dependence on informal sources of credit.

(vi) It is important that the formal credit is distributed more equally so that the poor can benefit from the cheaper loans.

51. “Poor households still depend on informal sources of credit.” Support the statement with examples.

View AnswerAns. (i) Banks are not present everywhere in rural India. Even when they are present, getting a loan from a bank is much more difficult than taking a loan from informal sources.

(ii) Bank loans require proper document and collateral. Absence of collateral is one of the major reasons which prevents the poor from getting bank loans.

(iii) Informal lenders such as moneylenders, on the other hand, know the borrowers personally and hence are often willing to give a loan without collateral. The borrowers can, if necessary, approach the moneylenders even without repaying their earlier loans.

52. “The credit activities of the informal sector should be discouraged.” Support the statement with arguments.

View AnswerAns. The credit activities of the informal sector should be discouraged because:

(i) About 85% of loans taken by the poor households in the urban areas are from informal sources.

(ii) Informal lenders charge very high interest on their loans.

(iii) There are no boundaries and restrictions.

(iv) Higher cost of borrowing means a larger part of the earnings of the borrowers is used to repay the loan.

(v) In certain cases, the high interest rate for borrowing call mean that the amount to be repaid is greater than the income of the borrower.

(vi) This could lead to increasing debt and debt trap, therefore the credit activities of the informal sector should be discouraged.

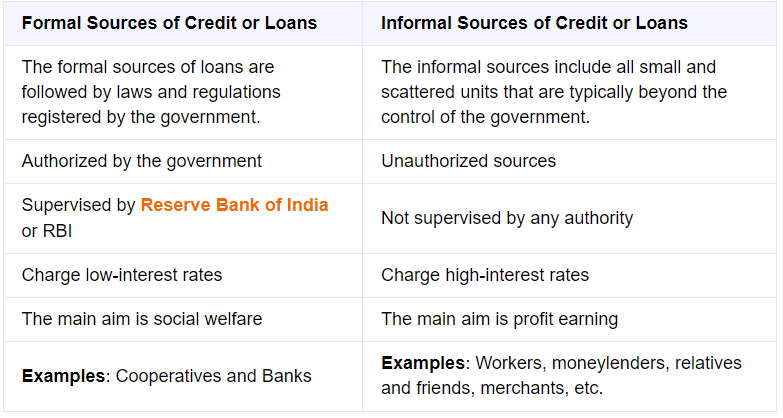

53. Explain the differences between formal and informal sources of credit.

OR

Mention three points of difference between formal sector and informal sector loans.

View AnswerAns.

54. How can the formal sector loans be made beneficial for poor farmers and workers? Suggest any five measures.

OR

Why are formal sources of credit preferred over the informal source of credit? Give three reasons.

View AnswerAns. Formal sector loans can be made beneficial for poor farmers and workers in the following ways:

(i) Create awareness to farmers about formal sector loans.

(ii) Process of providing loans should be made easier.

(iii) It should be simple, fast and timely.

(iv) More number of nationalised banks/cooperative banks should be opened in rural sector.

(v) Banks and cooperatives should increase facility of providing loans so that dependence on informal sources of credit reduces.

(vi) The benefits of loans should be extended to poor farmers and small scale industries.

(vii) While formal sector loans need to expand, it is also necessary that everyone receives these loans.

55. Which are the two major sources of formal sectors in India? Why do we need to expand the formal sources of credit?

View AnswerAns. The two major sources of formal sources of credit are:

(i) Banks and (ii) Cooperatives.

Need to expand formal sources of credit are:

(i) To save the poor farmers and workers from the exploitation by the informal sector credit.

(ii) Informal sector charges a higher interest on loans which means that a large part of the earnings is used to repay the loan.

(iii) Formal credit can fulfil various needs of the people through providing cheap and affordable credit.

56. What are the drawbacks of informal sources of credit?

OR

“The credit activities of the informal sector should be discouraged.” Support the statement with arguments.

View AnswerAns. (i) Most of the informal lenders charge a much higher interest on loans. Thus the cost to the borrower of the informal loans is much higher.

(ii) Higher cost of borrowing means a larger part of earning of the borrowers is used to repay the loan and they have less income left for themselves.

(iii) The high rate of interest of borrowing can mean that the amount to be repaid is greater than the income of the borrower and it can lead to increasing debt and debt-trap.

(iv) People who might wish to start an enterprise by borrowing may not do so because of the high cost of borrowing.

57. What is the role of SHGs? What are the reasons of its growing popularity?

OR

What are Self-Help Groups? Describe, in brief, their functioning.

View AnswerAns. Self-Help Groups (SHGs) have 15 to 20 members and pool their savings and after some time, it becomes a large amount which is used to give loans to the needy ones at a very nominal rate of interest. Its role:

(i) Help to reduce the functioning of informal sectors of credit.

(ii) Able to create self-employment opportunities for the members.

(iii) To organise rural poor particularly women and pool their savings.

SHGs are becoming popular for the following reasons:

(i) They help borrowers overcome the problem of lack of collateral.

(ii) They can get timely loans for variety of purposes and at a reasonable interest rate.

(iii) They are building blocks of the organisation of the rural poor.

(iv) It helps women to become self-reliant.

(v) The regular meetings of the group provide a platform to discuss and act on various social issues such as health, nutrition, domestic violence, etc.

58. Self Help Groups’ help borrowers to overcome the problem of back of collateral. Examine the statement.

View AnswerAns. (i) In a self-help group most of the important decisions regarding the savings and loan activities are taken by the group members.

(ii) Group members are well known to each other. They belong to the same society.

(iii) Also, it is the group which is responsible for the repayment of the loan.

(iv) Any case of non-repayment of loan by any one member is followed up seriously by other members in the group.

(v) Due to this feature, banks are willing to land to the poor women when organised in SHGs, even though they have no collateral as such.

Thus, through the above points, we can easily say that the Self-Help Groups help borrowers to overcome the problem of back of collateral.